CHEAT SHEET

- Public roads. The earliest wave of autonomous vehicle legislation (in California, Florida, and Nevada) was concerned with the safe operation and testing of self-driving cars. While 21 US states and the District of Columbia have approved the use and testing of autonomous vehicles, more than half have not given the green light.

- Smart cities. Autonomous cars are only as smart as their surroundings allow, and today’s urban landscape is decidedly ill-prepared for the tech infrastructure necessary for next generation vehicles. Unless lawmakers establish who will bear the burden of this cost, the tech infrastructure will remain fragmented.

- Opportunities abound. In the same way that autonomy brings policy concerns, it also creates new job opportunities, highway safety potential, and land-use considerations.

- French initiative. The French government are at the vanguard of autonomous vehicle testing. The government allowed car companies to test driverless cars on public roads in 2016, and French firms are leading the world in developing driverless public transportation.

More than a century after Carl Benz produced the world’s first gasoline-fueled, four-stroke cycle engine in 19th century Germany, the world waits for what technologists believe will be the swiftest and most radical disruption of transportation in the modern era: a truly “auto” mobile.

This seismic shift toward automotive autonomy will end what was once an exclusively human function, and with it invalidate the carefully curated, 100-year-old matrix of federal, state, and local laws and regulations that govern manual driving today.

The technology has high hopes to be one of the most transformative technological shifts in the modern era. Indeed, as cars mature into both a cleaner and smarter mode of transport, road fatalities will plummet (2016 was the deadliest traffic year in a decade, according to federal data) and road congestion will evaporate (platooning technology will allow for fast-moving, closely tracking streams of cars) — that’s the idea, at least.

But while technologists work daily to demonstrate (to regulators, to investors, and to consumers) the road-readiness of autonomous vehicles, the actual rhythm of the shift to widespread autonomy is one that will be dictated first by public policy and second by science.

It’s on this question — when America will become driverless — that government will exert the singularly decisive force: how and when policymakers address safety, cybersecurity, licensing, and liability considerations will either speed or stall the autonomous revolution.

Autonomous vehicles learn by doing and, in some cases, by failing. The question then becomes: Will governments abide by the wide berth required to test, develop, and deploy the next generation of cars on public roads?

State audit

Historically, the US federal government has regulated the vehicle while leaving the regulation of the driver to the states. But in the case of highly autonomous vehicles, the vehicle itself functions as the driver, blurring the once clear delineation of regulatory responsibility between state and federal government.

To date, no federal legislative framework for autonomous vehicles exists. It’s in that regulatory vacuum that state legislative and rule-making bodies have begun to develop fragmented and sometimes conflicting laws governing the testing and licensing of autonomous vehicles. And it’s within this messy context that auto manufacturers have begun testing experimental vehicles.

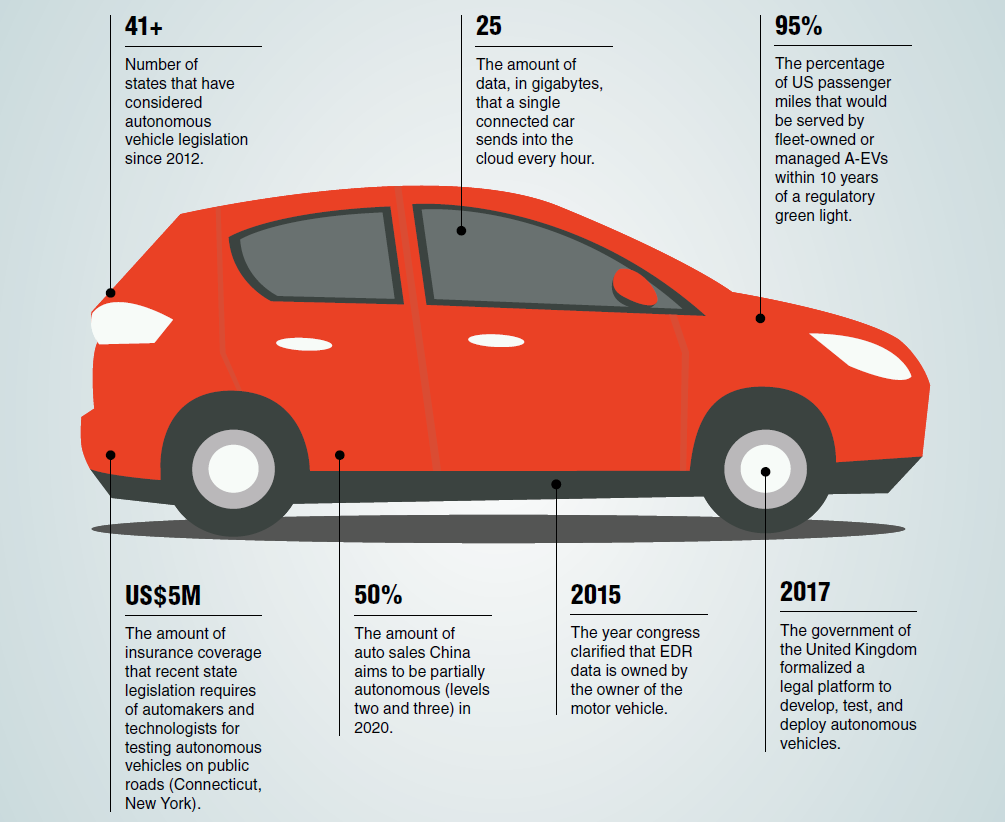

Since 2012, at least 41 US states and the District of Columbia have considered autonomous vehicle legislation. Of them, 21 have passed frameworks, while governors in another four states have issued executive orders. Their primary concerns included:

Operation on public roads: The earliest wave of autonomous vehicle legislation (in California, Florida, and Nevada) was concerned with the safe operation and testing of driverless cars. These bills predated the earliest policy guidance by federal regulators or legislative action by Congress, setting a loose standard for successive states to adopt. In the broadest terms, these states required those testing autonomous vehicles to notify state regulators and in some cases receive special licensing pending vehicle inspection. Some states dictated strenuous black box-like data capture, storage, and transmission requirements for experimental AVS, while others set requirements for operators (i.e., that they be present for safety fallbacks, or that they be qualified engineers). While 21 states and the District of Columbia have approved in some way the use and testing of autonomous vehicles, more than half have not given the explicit green light.

Insurance and liability: The most recent wave of state legislation has been marked by a requirement that automakers and technologists who are engaged in the testing of autonomous vehicles on public roads provide proof of insurance of at least US$5 million (Connecticut, New York). Because most of the earliest autonomous vehicles were belatedly retrofitted for the purpose of driverless cars by a third party, early states (DC, Nevada, and Michigan) to address liability explicitly freed manufacturers from some liability concerns when a car had been altered after-market. More recently, though, as automakers themselves have begun producing and testing highly autonomous vehicles, state lawmakers have placed liability with car makers, assuming that the automated driving system was in operation at the time of the accident.

Commercial motor vehicles: Since 2012, eight states (Arkansas, Georgia, Michigan, Nevada, North Carolina, South Carolina, Tennessee, Texas, and Florida, which commissioned a blue ribbon panel) have passed laws that would make a special dispensation for commercial, non-leading motor vehicles from existing following-too-closely laws. Generally, the bills defined a coordinated commercial platoon as a group of autonomous heavy trucks traveling bumper-to-bumper under the control of a single human operator in a lead vehicle. In practice, the easing of rules allows the tethering of multiple large trucks into a single, digitally married unit.

Six tiers of autonomy

SAE International, formally known as the Society of Automotive Engineers, rates automotive autonomy on a six-tiered, graduated scale.

Level zero, no automation: Full-time performance by a human driver of all aspects of all driving tasks.

Level one, driver assistance: A driver assist system of either steering of acceleration and deceleration coupled with requirements that a human driver perform the remaining dynamic tasks. Examples include adaptive cruise control or park assistance.

Level two, partial automation: Driver-assist systems control both steering and acceleration and deceleration by intelligently processing environmental information while the human driver performs remaining dynamic tasks.

Level three, conditional automation: Automated driving systems perform all aspects of the driving task, with the expectation that a human driver will respond and intervene when and where necessary.

Level four, high automation: Performance by an automated driving system of all aspects of the driving task within defined geographic cordons (i.e., college campuses or business districts).

Level five, full automation: The full performance of driving by an automated driving system under all roadway and environmental conditions. Human intervention is not required, so conventional aspects of the car (steering wheel, pedals) are removed.

Federal audit

Traditional rule-making is a slow process, sometimes stretching as long as eight years, but the National Highway Traffic Safety Administration (NHTSA) has shown an eagerness to access more expedient tools to help shape the future of autonomy even and especially as the states have begun developing individual safety systems. In 2016, it released what the agency billed as policy guidance for states and automakers. But compliance with the guidance, which included a 15-point safety threshold for manufacturers and testers, was merely voluntary.

Fearful the increasingly fragmented state legislative landscape would wither the appetite of automakers to continue operating in regulatory gray zones, the US House of Representatives in September 2017 adopted a bipartisan proposal to empower (and prod) NHTSA to formalize new federal safety rules for the use of autonomous vehicles. The new law, which has cleared the lower chamber and awaits Senate consideration, would pointedly preempt state rules and additionally carved out special exemptions for experimental vehicles that don’t satisfy current federal motor vehicle safety standards, which have fallen so far behind contemporary technology that they still require the presence of a driver and conventional driving systems like a steering wheel and acceleration and deceleration pedals.

Major automakers like Ford Motor Company have pledged to mass produce highly autonomous vehicle models that lack steering wheels, but the pace of that technology ultimately going to mass market is one that will be dictated in Washington and not Silicon Valley. Because the technology has sped so far ahead of existing law and regulation, policymakers will command outside influence in the coming process, understanding that a dramatic refresh of federal safety rules and those laws governing driver and manufacturer liability, cybersecurity, federal subsidies, and data privacy is required.

Policy must-resolves include:

- Smart city and connected car (V2X) data infrastructure requirements and investments;

- Cybersecurity standards, privacy, breach punishments, and liability;

- Federal subsidies for automakers, early consumer adopters;

- Autonomous commercial motor vehicle regulations;

- New safety standards, and conditional carve-outs for experimental testing;

- Data privacy: what will be shared, with whom, in what ways will it be made available, and to what ends;

- Accident liability: in cases of instrument malfunction or flaw, how can policymakers assign liability to manufacturers without crushing incentive to invest in the nascent technology and industry;

- Decarbonization incentives for automakers and consumers;

- Removing barriers to ride-sharing, interstate fleet management; and,

- Encouragement of open-data mapping platforms.

In particular, the questions of retrofitting our municipal transportation system to accommodate smart cars and of vehicle data control and ownership are among the most pressing before federal lawmakers.

Auto technology industry complaints

In the last 18 months, the industry has begun aggressively lobbying federal lawmakers for a single set of federal standards, arguing that the patchwork of state rules would ultimately harm the testing and market scaling of autonomous vehicles. Compliance when each state has varying testing systems, the companies protested, would slow the ability to test in varying climates and development zones (urban vs. rural highway vs. city street).

Smart cities make smart cars

Despite the billions spent in research and development for the parts and artificial intelligence required to make a driverless car drive, it will take a smart city for autonomous cars to be truly smart.

Autonomous cars are only as smart as their surroundings allow, and today’s urban landscape is decidedly ill-prepared for the tech infrastructure necessary for the next generation of vehicles. The data that autonomous cars will receive and transmit both within and without other cars will be staggering, and few cities have the resources to retrofit traffic control systems for vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications.

Unless and until lawmakers establish who — cities, states, the federal government, or original equipment manufacturers (OEMs) — will bear the burden of this cost, possibly in an omnibus infrastructure bill, the tech infrastructure landscape will remain sharply fragmented.

With great data comes great responsibility

In the same way that today’s cars run on oil, tomorrow’s will run on data. Consider: a single connected car will lob some 25 gigabytes of data to the cloud every hour while the average wireless customer consumes just 1.8 GB in a month.

As the first-generation sensors, radars, V2V, V2I, and mapping programs that operate today’s autonomous cars mature into more advanced systems, so too will the data they consume expand exponentially.

To date, the issue of vehicle data and control thereof (whether it’s personal, geo-positional, or operational) has only been addressed in federal law with respect to event data recorders (EDRs). In 2015, Congress clarified that EDR data is owned by the owner of the motor vehicle.

In Europe, original equipment manufacturers have argued that the data is theirs to use, and many believe they will attempt to chart a similar course in the United States. On a global basis, how, where, and when that data is accessed and for what purposes and by whom is one of the biggest potholes in the autonomy landscape.

Transportation as a service

The car of the future will be green, safe, and connected, but some technologists and data scientists have begun positing that it won’t be individually owned. Instead, the car of the future could be part of a roving ride-sharing fleet.

This hypothesized shift from individually owned and maintained internal combustion engine (ICE) vehicles to fleet-owned or managed electric autonomous vehicles (E-AVs) has been dubbed “transportation as a service” (TaaS).

One study held that within 10 years of the regulatory green light for autonomous vehicles, some 95 percent of US passenger miles would be served by fleet-owned or managed A-EVs. Leveraging TaaS would be four to 10 times less expensive per mile than operating a paid-off vehicle by 2021, the same study estimated, in part because utilization rates would be dramatically higher for A-EVs, which would require far lower maintenance, energy, and insurance-related costs.

Global activity

ASIA

China aims to have partially autonomous cars (levels two and three) account for 50 percent of all auto sales in 2020; for highly autonomous cars (level four) to account for 15 percent of sales in 2025; and fully autonomous cars (level five) to account for 10 percent in 2030. Annually, that would mean some four million robotic cars.

In Japan, the government and business community are furiously laying the legal and technological framework to make its capital city truly autonomous in time for the 2020 Summer Olympic Games. Already, technology firms have begun intensive 3D mapping of the country’s roadways (recording details as minor as curb height), some 20 times more precise than current maps.

EUROPE

Home to many of the world’s largest car makers, Germany’s parliament recently advanced a framework allowing for the testing of autonomous vehicles on public roads (with the requirement that a human operator must remain at the ready to resume control of the vehicle). In 2017, the government of the United Kingdom formalized a legal platform to develop, test, and deploy autonomous vehicles. Notably, the bill included a driver liability plank, holding drivers at fault even when self-driving is enabled if the driver has modified the car’s software or failed to install critical updates. Insurance will be needed both when the driver is in manual control and when the car is operating autonomously. The government has licensed eight narrow tests, including a four-seater autonomous bus pilot on a shared cyclist and pedestrian route in London, and will commence two on public roads in 2017.

French government and industry are at the vanguard of autonomous vehicle testing. The government allowed car companies to test driverless cars on public roads in 2016, calling the shift to autonomy a public safety necessity. In particular, French firms are leading the world in developing driverless public transportation.

NORTH AMERICA

Canada is notably lagging all other G7 nations in developing legal and regulatory frameworks for the testing and commercial deployment of autonomous vehicles. One Canadian technologist was quoted by the Financial Post as calling the country “dead last” among the G7 in preparing for autonomy. Under current law, a vehicle without a steering wheel and pedals would not be allowed on public roads.

New opportunities, challenges for local governments

In the same way that the successful shift to autonomy first requires the resolution of outstanding public policy concerns, so too does the successful shift create new questions on tax policy and incentives, land use and redevelopment, infrastructure funding, and spending priorities for the federal government, as well as cities and states.

Revenue shortfalls

Electric autonomous vehicles would short circuit a profound source of revenue for state government: the gas tax. How can state and local governments find an equitable solution to address the likely shortfall because electric car owners won’t pay tax on gas they don’t purchase? Every vehicle and mode of transportation should be treated fairly, a balanced equation related to its usage of public space and impact on congestion and pollution.

Jobs

Electric autonomous vehicles, if taken to scale, will exert tremendous (and, in some cases, indirectly negative) influence on downstream jobs, including those working in the energy sector, as professional drivers, and in convenience stores. How will cities and states retrain these workers?

Land bonanza

The city of Los Angeles boasts 200 square miles of parking space, an area large enough to accommodate three cities the size of San Francisco. If the personal transportation paradigm shifts from personal car ownership to participation in shared fleets that are available on-demand, how can cities repurpose this land?

Financing and insurance

TaaS, and its associated changing business models of fleet ownership, fleet management and accident liability will have a profound impact on the financial services industry associated with automobiles. Financial markets will also need to rethink how automobiles and autonomous fleets are financed and insured. Autonomous vehicles also promise rapid increases in highway safety, and the resulting changes in insurance premiums and the insurance industry have yet to be fully considered by lawmakers and regulators.

Like the American West of the early 19th century, makers of autonomous vehicles have operated for the last few years in a regulatory-free wilderness, rarely feeling nor seeing the hand of the law. But as the technology has increasingly captured the imagination of the public, so too has it drawn the interest of lawmakers.

Not since Benz’s four-stroke engine and the early boom of car sales has transportation so dramatically outpaced regulation. The consideration of red tape — when, where, and how much to unfurl on industry — is often balanced against its possible harm. In the case of autonomous vehicles, though, regulation is needed to prevent industry harm and ensure consumer protection, all while encouraging commercial innovation. Federal, cohesive, and responsive rules will speed the United States into the driverless era.

The authors would like to thank Tim Banks for his contributions to this article.