On the eve of International Women’s Day in March 2017, a statue of a small but defiant girl appeared opposite the famous Charging Bull sculpture on Wall Street. The statue was commissioned by the financial firm State Street Global Advisors to draw attention to the power of, and the lack of, women in business. These disparities are often highlighted in the corporate boardroom.

In 2010, the Alliance for Board Diversity found that 84.3 percent of all Fortune 500 corporate board seats were held by men. By 2018, that number had decreased slightly to 77.5 percent. Of those men, an overwhelming majority were white. In light of these statistics, it is no surprise that the focus on diverse representation on corporate boards has increased in recent years. This momentum has been further spurred by a widespread informed consensus that success in inclusion and diversity is a source of competitive advantage and a key enabler of growth. According to a 2018 report from McKinsey & Company, companies in the top quartile for gender diversity on executive teams were 21 percent more likely to outperform on profitability, and companies in the top quartile for ethnic and cultural diversity on executive teams were 33 percent more likely to have industry-leading profitability. This article examines current trends with respect to board diversity in the United States (US), as they contrast with developments in Europe. Overall, the movement to meaningfully implement board diversity in the US continues to grow apace.

European quota model

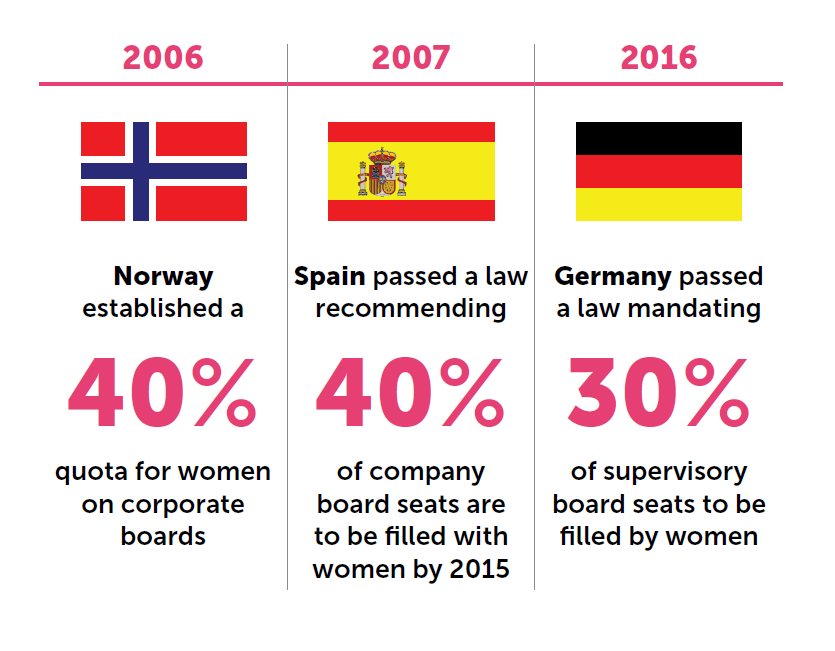

Unlike the US, European countries have largely sought to solve the diversity issue through political and governmental action, primarily in the form of quotas for women on corporate boards. Norway, for example, established a 40 percent quota in 2006 and reported to have achieved this target in 2008. Spain passed a law in 2007 recommending that companies fill 40 percent of their board seats with women by 2015. In 2016, Germany passed a law mandating 30 percent of supervisory board seats be filled by women, becoming the largest economy to impose a quota. In the UK, the February 2015 Davies Report’s review, “Women on Boards,” recommended that FTSE 350 companies should aim for at least 33 percent female representation on boards by 2020. On a pan-European level, in 2012 the European Parliament approved, by a strong majority, an EU-wide directive with a 40 percent quota for listed companies by 2020. The European quota system has ostensibly achieved its goal of improving female representation in boardrooms, as the number of women non-executive board members at the largest listed companies across Europe in 2018 was at 29.3 percent, up from 11 percent in 2007, according to the European Institute for Gender Equality. The most significant progress, however, tends to be concentrated in a few member states while other states have seen minimal progress, or even a decrease in board diversity.

Diversity and the US federal government

While regulatory developments with respect to board diversity in Europe have focused on the inclusion of women on corporate boards through quotas, in the US, the regulatory focus has been on public disclosure. Take, for example, the Securities and Exchange Commission’s (SEC) rules that govern the disclosures required in a company’s annual proxy statement. Regulation S-K requires a company to “briefly discuss the specific experience, qualifications, attributes or skills that led to the conclusion that the person should serve as a director.” Furthermore, companies are required to disclose whether diversity is considered by the nominating committee in nominating directors, and if so, how it impacts the nomination process. Additionally, if the nominating committee or the board has a policy regarding the consideration of diversity in identifying director nominees, the rules require disclosure of how this policy is implemented and how the nominating committee or the board assesses the effectiveness of its policy. The SEC has declined to define diversity, rather leaving it to the company to define the term as broadly or narrowly as deemed appropriate.

In February 2019, the SEC staff (Staff) issued new guidance encouraging public companies to provide details on how they consider diversity when making decisions regarding the makeup of their boards and clarifying existing disclosure requirements. The Staff stated that to the extent a board or nominating committee considers a board member’s or nominee’s diversity characteristics “such as their race, gender, ethnicity, religion, nationality, disability, sexual orientation, or cultural background,” the Staff expects the company to identify those characteristics and how they were considered. Similarly, when a public company discusses its process for identifying director nominees, it should disclose how self-identified diversity attributes are considered “as well as any other qualifications its diversity policy takes into account, such as diverse work experiences, military service, or socio-economic or demographic characteristics.” This guidance provides public companies with a roadmap to explain how they factor diversity into nomination decisions and other corporate policies.

Beyond these disclosure rules, there are no other federal regulatory or legislative requirements specifically addressing corporate board diversity. Recently, however, the “Improving Corporate Governance Through Diversity Act of 2019” was introduced in both houses of Congress, garnering the support of the US Chamber of Commerce and the Council for Institutional Investors. If passed, this bill would enhance the SEC disclosure rules by requiring public companies to disclose in their annual proxy statements the gender, race, ethnicity, and veteran status of their directors, director nominees, and senior executive officers. Public companies would also have to disclose the adoption of any board policy, plan, or strategy to promote racial, ethnic, and gender diversity. In addition, the bill directs the SEC’s Office of Minority and Women Inclusion to publish best practices for corporate reporting on diversity.

A shift toward a European model at the state level

At the state level, laws and resolutions have recently been passed to tackle the issue of boardroom diversity, indicating a possible shift toward the European model. In 2018, California passed a law requiring public corporations incorporated or headquartered in the state to include a certain number of female directors on the board, becoming the first state to adopt gender quotas for boardrooms. The act requires boards, by the close of 2021, to have a minimum of one female director, with additional female directors required for larger boards. Similarly, legislation was introduced in New Jersey that would require public companies based in the state to appoint at least one female director by 2019, and then build on that requirement based on each corporation’s total number of board members by 2021.

While California and New Jersey have elected to impose formal quotas, several other states have passed nonbinding resolutions encouraging corporations to diversify their boards. For instance, a regulation encourages all Massachusetts corporations to adopt policies and practices designed to increase gender diversity on their boards, and to publicly disclose the number of women on their boards. In Illinois, a resolution encourages publicly held corporations with at least nine directors to include at least three women, with additional requirements for larger boards. Pennsylvania passed a resolution urging every corporation in the state to reach a minimum of 30 percent women directors by 2020 and to publicly track their progress toward this goal on an annual basis.

It remains unclear whether more states will enact binding measures to encourage corporate board gender diversity. Proponents of quotas argue that they are the quickest and most effective way to ensure more equal numbers of men and women on boards, and that they have an important ripple effect, namely that the increase in female directors will ultimately help steer the hiring and promotion of more women across the corporation. Regardless, quotas remain controversial as a solution to board diversity because they limit board discretion to determine appropriate board nominees based on the corporation’s needs. Additional criticisms are that female directors under a quota system could be seen as token and less deserving of the position, and that quotas may lead corporations to view them as a ceiling rather than a floor, stalling progress on equality in the long run. In addition, state laws may face constitutional challenges.

Peer pressure: Institutional investors weigh in

As they have with many recent corporate governance initiatives, institutional investors in the US have largely driven the movement toward corporate board diversity. Many institutional investors and proxy advisory firms, whose influence over corporate boards is ever-increasing, have developed diversity policies to guide investment and corporate governance decisions, applying considerable pressure on boards to promote diversity.

Key asset management firms have become catalysts for change, leading the way for greater gender diversity on boards. In February 2018, BlackRock, Inc., the world’s largest asset manager, issued its updated proxy voting guidelines emphasizing its expectation to see at least two female directors on every US public company board, and indicated that it may vote against corporate governance and nominating committee members “to the extent that [BlackRock believes] that a company has not adequately accounted for diversity in its board composition.” In 2017, William McNabb, chairman of The Vanguard Group, Inc., wrote in an open letter to directors of public companies worldwide that Vanguard will focus on gender diversity over the coming years, a matter it views as an “economic imperative.”

In its 2018 proxy voting guidelines, State Street Global Advisors emphasized its expectation to see a minimum of one female director on boards of companies listed on the Russell 3000 Index, and, in a 2018 press release, State Street announced that, beginning in 2020, it will vote against all members of the nominating and governance committee if a company does not have at least one woman on its board and has not engaged in successful dialogue on State Street’s board gender diversity program for three consecutive years. State Street reports that more than 300 companies have added a female board director in response to its demand and another 28 have pledged to do so.

Eversheds Sutherland signed the Mansfield Rule 2.0, which commits Eversheds Sutherland to having candidate pools for promotions, senior-level hiring, and significant leadership roles consist of at least 30 percent women, LGBTQ+, and/or minority lawyers. Committing to Mansfield 2.0 followed Eversheds Sutherland’s publicly stated goal of attaining 30 percent female partnership and 30 percent equity female partnership by 2021.

Some public institutional investors have adopted policies that explicitly promote board diversity. For instance, in March 2018, the California Public Employees’ Retirement System (CalPERS) identified board diversity as a “high priority initiative” and announced plans to vote against or withhold votes from directors at targeted companies that failed to take steps to add female directors. Similarly, the New York State Common Retirement Fund announced that it will oppose re-election of all directors at corporations with no female directors on the board and against corporate governance and nominating committee members at companies with only one female director.

Institutional investors have also taken active steps to encourage corporations to foster more diverse corporate boards. For example, Pax World Mutual Funds launched the Pax World Global Women’s Equality Fund, which invests in large cap companies that are leaders in promoting gender equality. One of the fund’s primary investment criteria is women’s inclusion both on the board of directors and in senior management.

In addition, major proxy advisory firms also have contributed to the effort to improve boardroom diversity. Beginning in January 2019, Glass Lewis will generally recommend voting against corporate governance and nominating committee chairs at corporations with no female board members. In 2018, Institutional Shareholder Services (ISS) began highlighting boards with no gender diversity. In November 2018, ISS announced that, starting in February 2020, it will generally recommend against the re-election of the nominating committee chair of a board with no female directors, and against other directors involved in the director nomination process on a case-by-case basis.

Despite the encouraging campaigns for diversity of many asset management and proxy advisory firms, the behavior of some institutional investors seems inconsistent with the pursuit to promote boardroom diversity. In particular, hedge fund activists seeking to change the composition of the corporate boards tend to put forward fewer diverse candidates. According to a 2017 study by ISS and the Investor Responsibility Research Center Institute, women made up only 8.4 percent of dissident nominees on proxy contest ballots and directors appointed through settlements with activists, and only 4.2 percent of dissident candidates and directors were ethnically or racially diverse.

A different option

With the urging of institutional investors, and in the absence of clear legislative and regulatory directives, some US companies have independently addressed gender diversity. The National Football League adopted a policy in 2003, called the Rooney Rule, requiring league teams to interview minority candidates for openings in high-level coaching and senior operations positions. The Rooney Rule also has extended into the realm of board diversity. For example, Facebook Chief Operating Officer Cheryl Sandberg announced in 2018 that the company would apply the Rooney Rule to board vacancies, publicly committing Facebook to interview a diverse slate of directors. Amazon similarly made a commitment to apply the Rooney Rule to vacancies on its board of directors after facing significant pressure regarding the adoption of a shareholder proposal on the topic. Other examples of high-profile companies who have adopted a form of the Rooney Rule include Uber, Costco, and Alphabet (the parent company of Google). While committing to interview a candidate is not the same as committing to place such candidate on the board, commentators see this as additional signs of the increasing pressure to meaningfully improve board diversity.

Conclusion

Although a range of theories is offered in support of promoting board diversity, proponents of board diversity frequently point to improved corporate performance and other market- or economic-based rationales when defending the merits of their position. Regardless of the theory that such proponents subscribe to, it is evident that the movement toward increased diversity on corporate boards of directors has become the corporate governance initiative du jour and is an issue corporations will have to contend with going forward. As a result, corporations may want to revisit their board diversity policies in connection with their annual director nomination processes and in the preparation of disclosures included in their proxy statements. In addition, corporations may wish to proactively engage institutional investors on the topic of board diversity.

The authors would like to thank Eversheds Sutherland Extern Constantine Flogaitis for his invaluable contributions to this article.

Further Reading

Lissa Broome, John Conley and Kimberly Krawiec, Dangerous Categories: Narratives of Corporate Board Diversity, 89 N.C. L. REV. 759 (2011).